Disability benefits are there for you if you need them.

Long-Term Disability

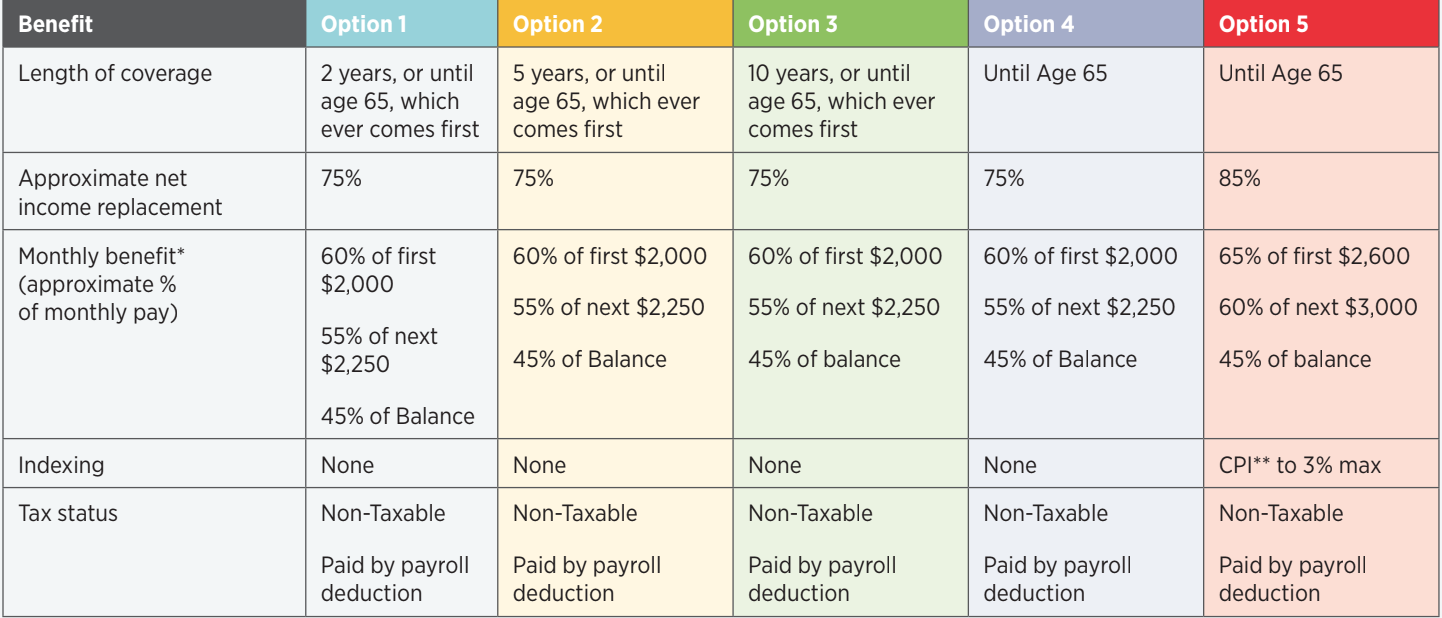

Long-term disability (LTD) coverage pays a monthly benefit if you are totally disabled and unable to work for more than 17 weeks. You have five options to purchase long-term disability coverage, as listed below.

")

{kind=link}